Ponzi Schemes Dropped In 2020, But That May Not Be A Silver Lining

(As a disclaimer, these statistics are presented for educational purposes only, have not been independently verified, and were primarily compiled through articles on Ponzitracker and reporting on the internet by various sources including Kathy Phelps' monthly Ponzi roundups at ThePonziSchemeBlog.com. Individuals accused of Ponzi schemes are presumed innocent until proven guilty. These statistics generally only included Ponzi schemes of around $1 million or more based in the United States. Please direct any comments or inquiries to inquiries@ponzitracker.com.)

Around this time last year, I wrote about how the annual data compilation showed an “ominous 30% surge” in the number of Ponzi schemes uncovered in 2019 as well as the “highest total amount of investor funds at issue in nearly ten years.” Although one year certainly does not create or make a trend, the surge in 2019 stopped a multi-year downward trend and also raised questions about whether the ensuing year (2020) would see the numbers creep back up to levels not seen in nearly a decade.

The answer is technically no, according to newly-compiled data for 2020 which showed a nearly-30% drop in Ponzi schemes during 2020. In a vacuum, this would be welcome news and a seemingly-resounding rejection of any hypothesis about the trend continuing from 2018. But the reality is that the world experienced unprecedented challenges and disruptions as civilization battled the scourge of COVID-19 during most of 2019, and these tribulations touched nearly all facets of life. The data suggests that financial fraud detection also experienced disruption, with the number of Ponzi schemes uncovered during the first half of 2020 marking the lowest six-month figure during the preceding 11-year period compiled by Ponzitracker. And as a result of many parts of the criminal justice system shutting down, the number of prison sentences handed down to Ponzi schemers also was the lowest on record during the last 11 years - by nearly 30%.

As the world slowly continues its climb back to a pre-COVID normalcy, there are multiple hints that 2020’s reversal may be an aberration owing to the pandemic’s paralyzing tentacles. These hints, including increased enforcement and outright warnings from regulators about an increase in consumer complaints, will be worth watching in the coming year.

2020 Ponzi Scheme Discoveries and Sentences

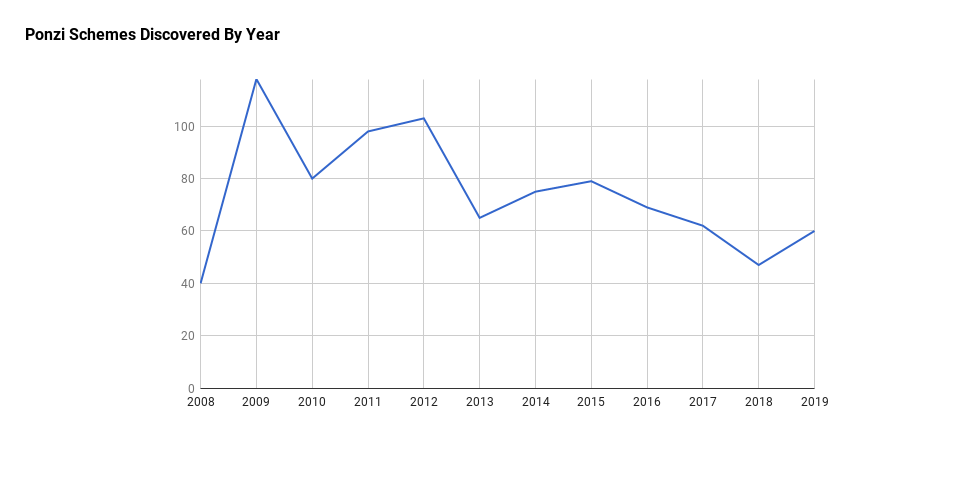

The beginning of 2020 came on the heels of a banner enforcement year in 2019 for regulators who uncovered at least 60 Ponzi schemes that collectively involved more than $3 billion in investor funds. But as murmurs of a unique illness became a deafening (and deadly) roar by late February, governments all over the world shut down and society shuddered to a halt.

In total, 46 schemes were uncovered in 2020, meaning that a new scheme was uncovered about once every eight days. Collectively, the 45 schemes represented roughly $1 billion in investor funds - down more than $2 billion from the $3.245 billion at issue in the schemes uncovered in 2019. Four of the schemes raised over $100 million each from victims, but the majority of schemes involved less than $10 million and resulted in an average scheme size of roughly $22.25 million - down over 60% from the $54 million scheme size seen in 2019. Nearly 1/3 of the accused Ponzi schemers called Florida or California home, but 2020 also saw smaller states like South Dakota, West Virginia, and Kentucky serve as home to an individual accused of a Ponzi scheme. One statistic that has remained remarkably consistent even in 2020? Men continued to make up nearly 90% of the accused Ponzi schemers.

The number of sentences handed down to convicted Ponzi schemers also saw a steep drop as courts grappled with closures and restrictions. Indeed, it appears that sentencing came to a halt during the middle of the year as the country employed strict measures to combat the pandemic. The data shows that there was a single sentence handed down during the period from March 1st to July 10th - the 25-year sentence imposed on radio host William “Doc” Gallagher (who called himself the Money Doctor) for his $20 million Ponzi scheme. The sentencings appear to have recently returned to the pre-COVID pace, but the total of 22 sentencings during 2020 mark a decade low..

Growing Hints Of Trouble Ahead

As the second surge of US infections began to decline in late summer, authorities brought civil or criminal charges against 20 suspected Ponzi schemers during the final four months of 2020 - representing an annualized total identical to the 60 discovered in 2019. While it remains to be seen whether this pace will continue given the ongoing surge in COVID cases, it does suggest that authorities have become more comfortable operating in the current environment and that a return to the near-standstill seen in the spring is unlikely.

One hint that this pace may continue? In mid-December, the Securities and Exchange Commission also issued a rare investor alert warning of “Investment Scam Complaints on the Rise.” These investor alerts and bulletins have historically been issued as routine updates or in connection with current cases or enforcement focuses. However, the December bulletin warned that :

The SEC has recently experienced a significant uptick in tips, complaints, and referrals involving investment scams. The SEC’s Office of Investor Education and Advocacy urges investors to be on high alert in order to protect themselves and others from becoming victims of investment fraud.

Ponzi schemes topped the SEC’s list of frauds to be on the lookout for, and affinity frauds also made the list.

Although there is no guarantee that the “significant uptick” in complaints involving investment scams will translate to an increase in enforcement actions involving Ponzi schemes, the reality is that the economy has enjoyed a remarkable and relatively consistent run over the past ten years since the Great Recession. The number of Ponzi scheme discoveries exploded in the wake of the Great Recession, and it can certainly be hypothesized that the next market downturn may lead to another large increase in discoveries. Regardless, it is still notable that the Commission decided an investor bulletin was warranted to disseminate this news - especially in the wake of the large market drop earlier in 2020 as the pandemic wreaked havoc on financial markets.

The database of alleged Ponzi scheme discoveries is below:

The sentences handed down in 2020 are below: